More anxiety, but not more data

The longest US government shutdown on record has finally ended, but it will take some time before the flow of statistical data releases resumes. When it does, it will initially be beset by unusual limitations. For instance, we should get the September employment report soon, but the one that we always said would matter more—the October one—may not be available at all. Or at least, the household survey portion of it, which would hold valuable information about the supply-demand dynamic in the labor market. Ever since the deferred DOGE layoffs in the spring, we penciled in a sizable negative print for October payrolls and an uptick in the unemployment rate. This should have left no doubt about a December Fed cut.

Instead, there are doubts aplenty, especially since the hawkish members of the FOMC (of which several are non-voters this year) have recently been out in force arguing against further cuts. From our vantage point, it feels that we’ve seen this scene not once, but twice before. First in the summer of 2024, when the FOMC turned quite hawkish on the basis of inflation fears before making a U-turn with 100 basis points of cuts on the basis of labor market concerns. The second time was this summer, when tariff/inflation concerns again delayed cuts until September. Given material relief in respect to tariff policy recently (China truce, Switzerland tariff reductions, seemingly imminent tariff reductions on key agricultural goods), one would presume that inflation concerns would be subsiding somewhat. And given the recent spike in private sector layoffs and multiplying headlines about further workforce reductions, one would simultaneously presume that labor market concerns should move up the priority list.

That doesn’t seem to necessarily be the case. Indeed, hawkish messaging from Fed officials drove market pricing for a December cut below 50% as of Friday the 14th. To some extent, it could be argued that a December and a January cut are interchangeable, so the Fed could wait till January. But if they are truly eyeing a January cut, then they might as well deliver it in December and recalibrate 2026 expectations in a more hawkish direction. Then, with three cuts under their belt, FOMC members can enter another extended pause to allow data to clarify the macro picture. This would be our preferred outcome, and we still believe this remains the most likely one. If new data in 2026 emphasize inflation concerns, the FOMC can blame the lack of data for the decision to cut in December. If instead it continues to emphasize labor market concerns, then the cut will be seen as that much more welcome and prescient. Seems like a win-win. Can the Chair convince the committee? We hope so.

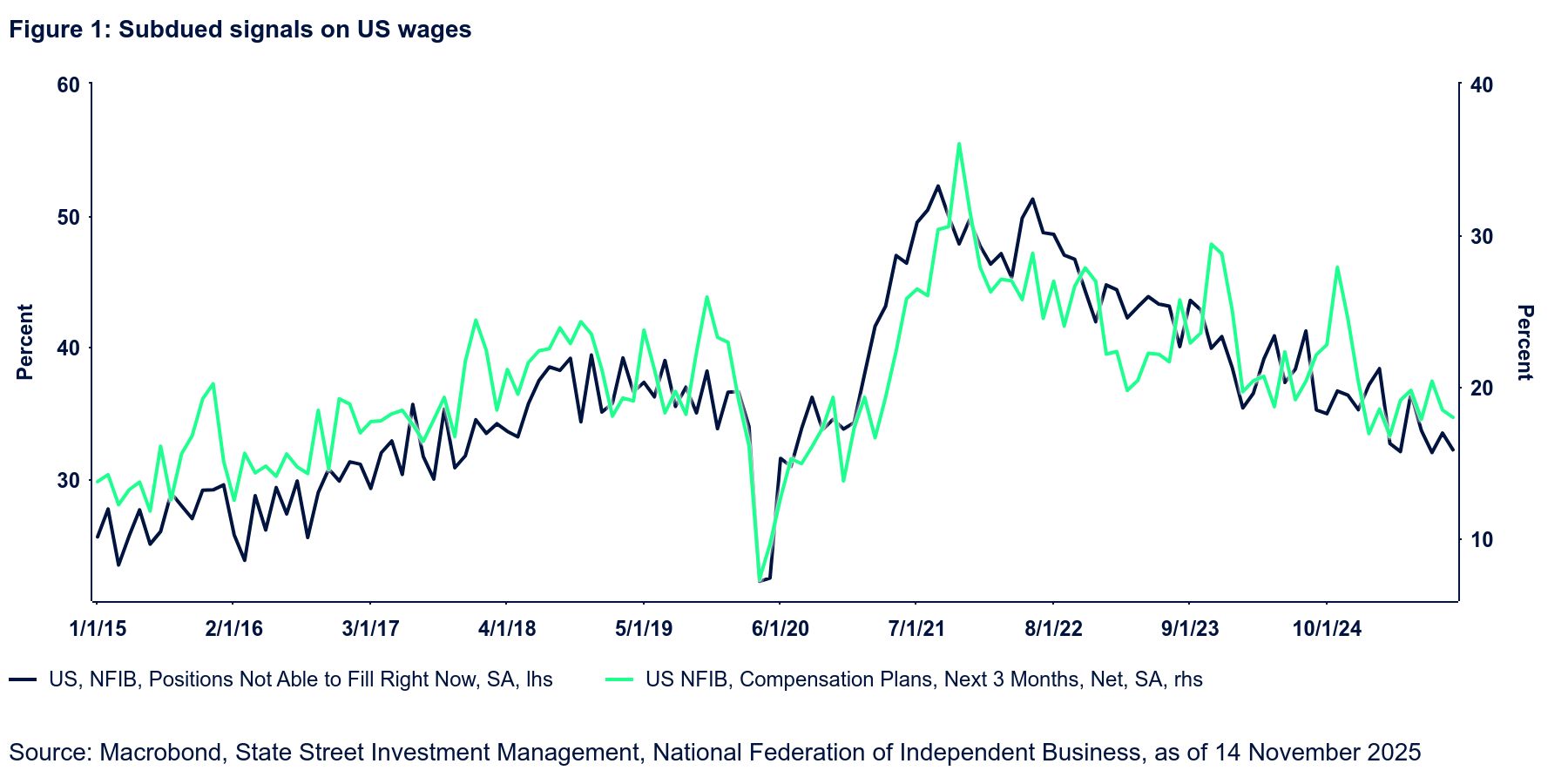

Whatever little data is still trickling in is not offering decisive takeaways. But there are repeated reassurance about the lack of inflationary pressures stemming from the labor market, and that should be an important consideration for policymakers.