September CPI data reinforces the case for two more Fed cuts in 2025

Good to go for back-to-back cuts

After an unusually long delay caused by the government shutdown, we finally got the September consumer price inflation data. It was fine. Better than expected, in fact, as both headline and core CPI inflation came in a tenth lower than the Bloomberg consensus. Overall prices rose 0.3% and the headline inflation rate quickened by a tenth to 3.0% YoY, while core prices rose 0.2%, allowing the core inflation rate to ease a tenth to 3.0% YoY.

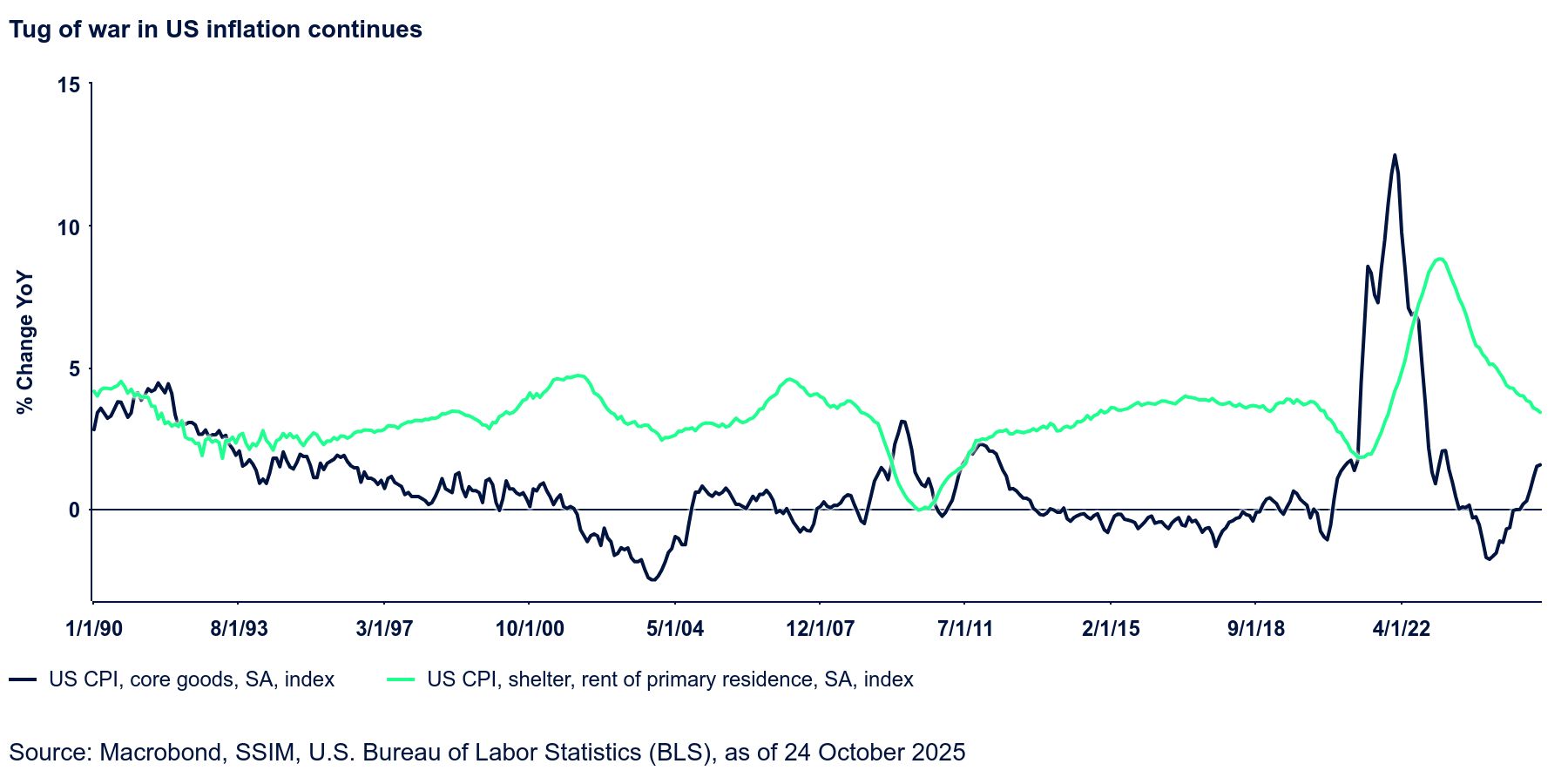

Energy commodities were a big contributor to the overall rise with a 3.8% MoM jump, but food prices (both at home and away from home) were well-behaved. Most importantly, shelter inflation continues to moderate. This offers a powerful disinflationary offset to the visible rise in goods prices because of tariffs. Rent of shelter costs increased 0.21% MoM, the second-smallest increase since February 2021, allowing this component of inflation to ease another tenth to 3.5% YoY. It has come down almost a full percentage point since January and now stands at the lowest level since September 2021. The good news is that given how backward-looking shelter inflation data is in the CPI report (methodology related), this gentle downtrend should continue throughout 2026. Core goods inflation is moving higher, but remains contained, suggesting modest passthrough from tariffs so far. Prices of non-durable commodities excluding food—where one may look for clear tariff impact—rose 1.8% MoM, the most since December.

The data should allow the Fed to cut at each of the remaining meetings this year, on October 29 and December 10.