Industrial revival afoot

Over the last several months, we’ve highlighted three main “sub-plots” in the broader US macro narrative: resilient growth, gradually easing inflation, and softening labor market.

To these, we can perhaps add another: a gradual yet unmistakable revival in industrial activity. After an extensive period of weakness spanning 2023–2024, US industrial production returned to positive YoY growth in January 2025. However, those gains did not cross above 1.0% YoY until last July. Since then, there has been a slight further uptrend, with output up 2.3% YoY in January 2026, the best print since September 2022.

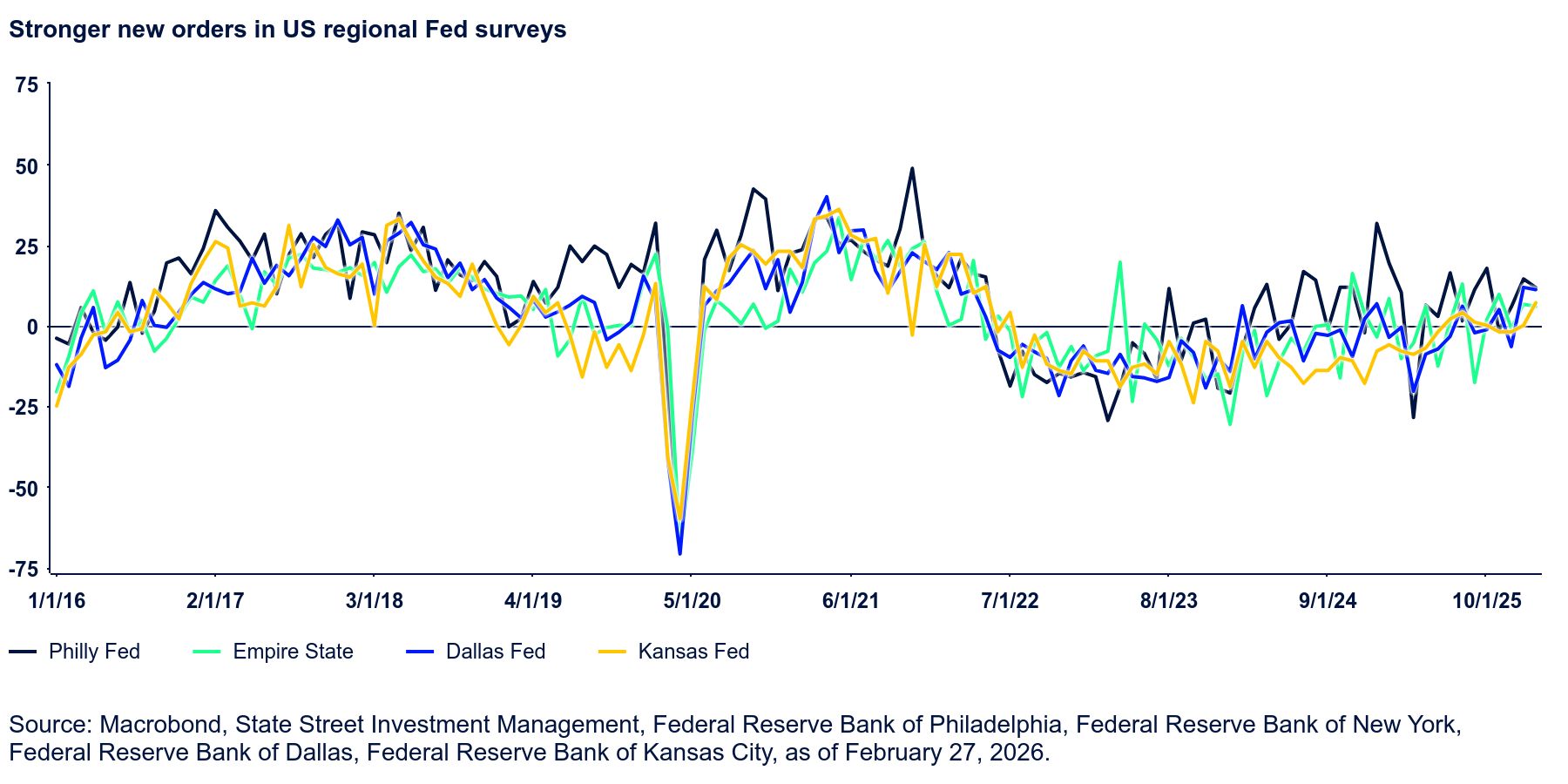

Recent data from various industrial and manufacturing surveys point to further gains in this space. Although not universal and, in some cases, volatile, the underlying signal from leading indicators such as new orders nevertheless remains one of improvement. Further gains in this space would certainly align with national policy priorities around strategic manufacturing resilience and could prove to be a lasting theme.

Unfolding hostilities in the Middle East are already pushing oil prices higher; if sustained, that could create an incentive for US energy producers to scale up output further, even as US oil production is already at a record.