New tariffs announced on April 2 leave the average US tariff rate at the highest level in a century (18.8% based on Tax Foundation estimates). The market reaction has been powerful but orderly so far, with risk assets globally sharply lower and bond yield falling. An extended period of negotiations lies ahead, with the trade war likely intensifying short-term through retaliation before agreements are eventually reached. But a 10% US universal tariff may have become the best case final outcome, save for Canada and Mexico, where closer integration is still our ultimate expectation.

The market response suggests this is, on net, viewed as a negative demand shock. Risk assets sold off sharply in the aftermath of the initial announcement and subsequent retaliatory action by China. US stocks experienced the worst two-day plunge since 2020, WTI oil prices dropped nearly $10 a barrel, and the yield on 10-year US Treasuries slipped to 4.0%, the lowest since mid-October. More Fed rate cuts are being priced in, with a June cut fully priced, more that two cuts priced by July and four by year end.

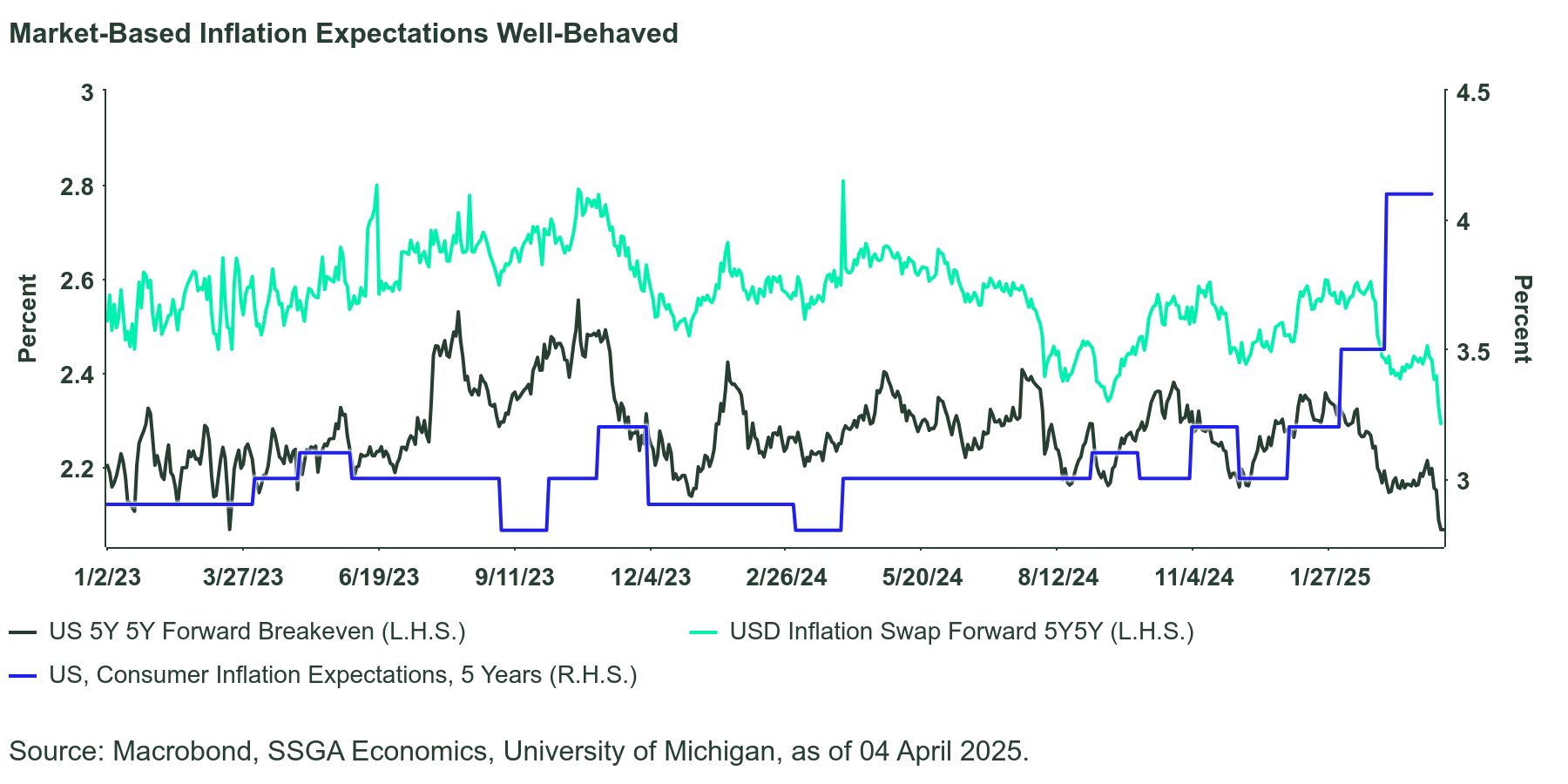

In contrast to a recent surge in consumers’ inflation expectations, market-based medium-term inflation expectations have been well behaved. Notably, they actually declined following the tariff announcement, suggesting investors see the inflationary impact of tariffs as short lived. This seems reasonable for two reasons:

a) Given that consumer wallets do not expand, higher tariffs cause a negative demand shock that eventually neutralizes the initial inflation effect.

b) On a longer term basis, the US policy of reshoring/friendshoring (which tariffs mean to accelerate) leads to additional productive capacity globally, without a commensurate increase in demand. Longer-tern, this is disinflationary.

No-Recession Call Is Hanging by a Thread

Since the start of the year, we have repeatedly argued that risks to both sides of the Fed’s dual mandate had increased. In our March forecasts (Little To See, Much To Worry About) we maintained a baseline macro call of slowdown but no recession, with real GDP growth moderating from 2.8% last year to 2.0% in 2025, driven primarily by softer consumer spending (2.8% to 2.2%, respectively).

The April 2 tariffs raise those risks to an “active threat” level. Relative to the March baseline forecast (which already incorporated tariff assumptions amounting to a roughly 0.4-0.5 hit to core PCE in H2 2025), we make further adjustments to those forecasts as follows: we raise end-2025 core-PCE inflation forecast by a further 0.3 ppt to 2.9% y/y, we lower Q4 2025 real GDP forecast by 0.2 ppt to 1.5% y/y, and we raise the end-2025 unemployment rate forecast by two tenths to 4.7%. We maintain the call for three rate cuts this year, although the rationale behind them has turned more ominous: no longer primarily a story of “cut because you can” but rather “cut because you have to”. While we do not have an outright recession in the forecast, we put the odds thereof at about 40%.

We retain the June-September-December timing despite risks of a later start.

Importantly, these forecast changes do not assume that these tariffs are permanent in their current form.

What Next?

Despite the detailed April 2 announcement, there is plenty we do not know. There will be retaliation (China has already made its move) but how intense? Most importantly, how long will US tariffs stay in place and what will their ultimate level be? It is impossible to know. But what we do know is that as they stand, these tariffs are too onerous to be sustainable without tipping the economy in recession. If in three month’s time these tariffs are still in place in their current form, the economy will be entering a recession. If they are scaled back (our baseline expectation), the no recession call might just survive by the barest of margins thanks partly to a decent starting point.

In that vein, the better than expected March employment report offered some reassurance, but not much since it reflects the past, rather than what is coming down the line. The economy added 228k jobs in March, much better than expected, although this was offset but a 48k downward revision to the prior two months. Gains were fairly well represented across sectors, although federal government employment and temporary help continued to shrink. The unemployment rate nudged up to 4.2% but this was primarily a rounding move and occurred alongside a one-tenth rise in the participation rate, so the dynamic was healthier than it appears at first glance. Hours worked were steady overall (up marginally in manufacturing) and wages well behaved. Average hourly earnings (AHE) inflation slowed to an eight-month low of 3.8% y/y while growth in average weekly earnings slowed to 3.2%. The latter is very important in constraining the extent of tariff passthrough. Given the consumer wallets are not expanding and job security is deteriorating, businesses may have difficulty passing through higher costs onto consumers, capping the ultimate inflation effect.