It is rare that the two marquee macro reports for the US economy—the employment and inflation data—are released in the same week. They were this week, and, at least on the surface, offered divergent signals on the state of the economy and the desired monetary policy path.

On one hand, the payrolls data was a clear upside surprise, coming in at 130k versus 65k expected. The unemployment rate ticked down a tenth to 4.3%, a five-month low and the underemployment rate dipped sharply to a six-month low of 8.0%. The hours worked and wages rebounded sequentially (MoM) after unusually weak December readings.

But these headline positive surprises were accompanied by yet another set of major downward revisions to the employment trajectory over the prior year, with employment at end-2025 roughly one million lower than prior estimates. To us, this is the bigger story, though we do not want to dismiss the stronger January data out of hand. Time will tell whether a genuine rebound in employment growth is possible, but we are a little suspicious of the big jump in healthcare/social assistance.

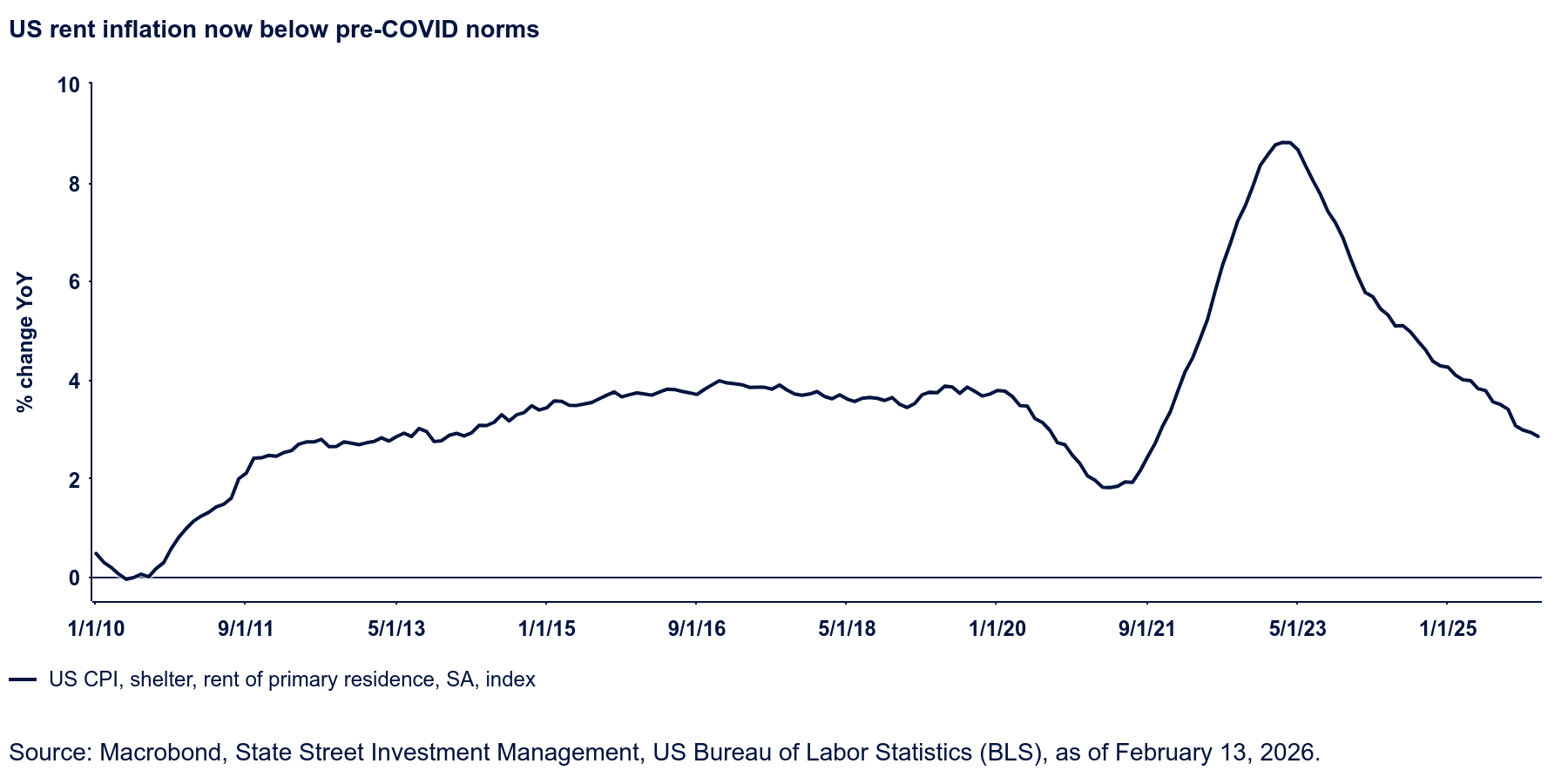

The market reaction to the employment report was, unsurprisingly, hawkish, with 10-year yields moving higher and odds of a June rate cut retreating. That didn’t last long, however. The inflation update on Friday showed fairly tepid price pressures, especially in the important shelter component, so the week ended on a dovish tone. Headline inflation eased three tenths to 2.4% YoY, a tenth more than anticipated; core inflation eased one tenth to 2.5% YoY. For the headline, this was the lowest level since May; for core, since March 2021!

This improvement reflects steady easing in shelter inflation, which more than offsets recent increases in core goods inflation. Given current market indicators of rent inflation, it is reasonable to anticipate further gentle easing in rent inflation over the next few months. Our end-of-year core-PCE forecast sits at 2.3% YoY in Q4, a little below the Fed’s 2.5% projection.