Stagflation signals

The first inflation report since the start of the Iran war showed the anticipated stark rise in headline inflation alongside contained core inflation.

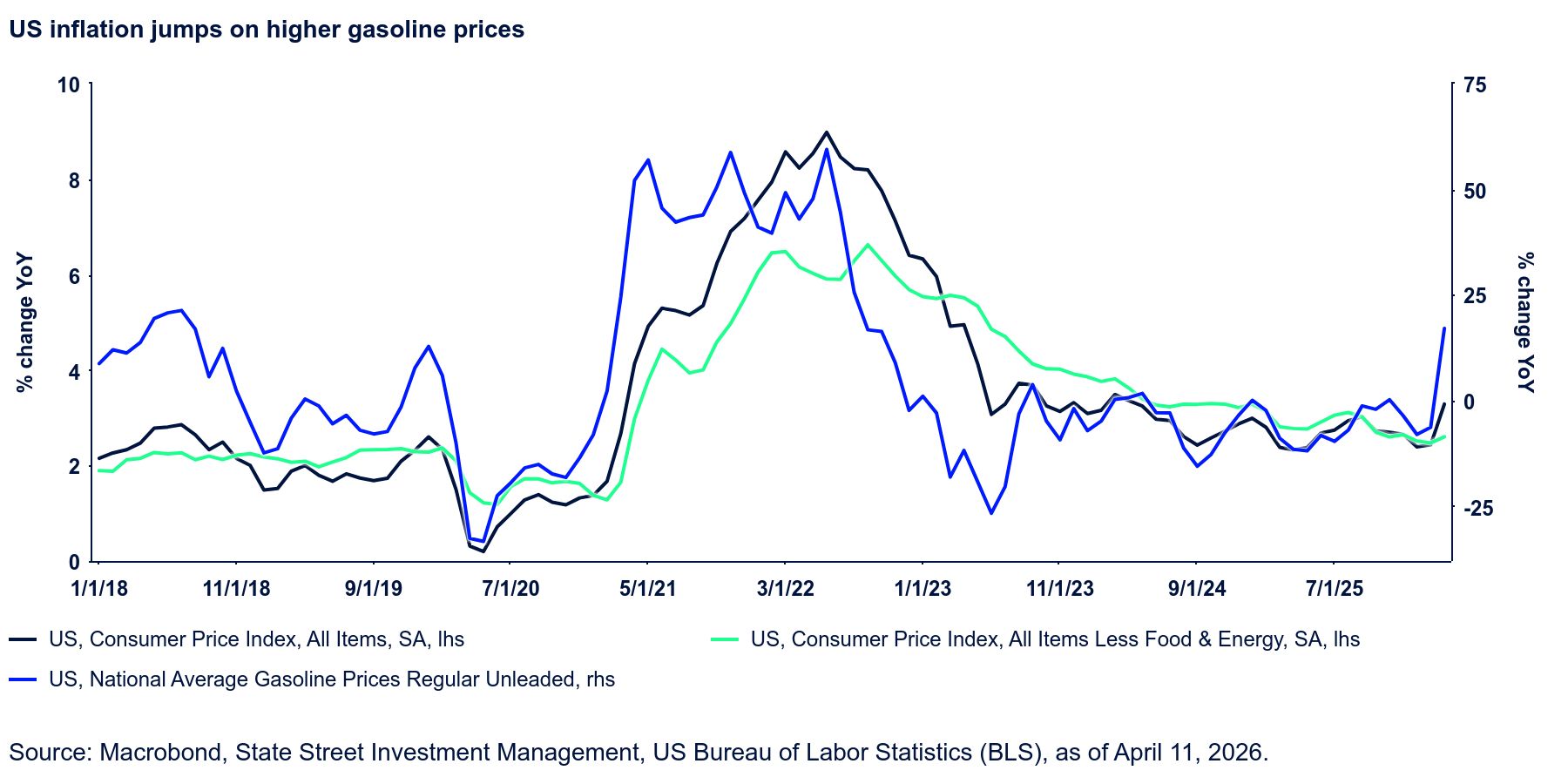

Overall consumer prices rose 0.9% MoM, lifting the headline inflation rate by 0.9 percentage points (ppt) to 3.3% YoY, the twin‑highest since May 2024. Core prices (excluding food and energy) rose 0.2% and the core inflation rate increased just one tenth to 2.6% YoY. Gasoline prices rose 21.2% MoM, food prices were unchanged, airfares increased 2.7% MoM, medical care declined 0.2% MoM and shelter rose 0.3% MoM. Overall, service prices increased 0.2% and goods prices jumped 2.0%.

None of this was surprising. What is surprising to us is the ongoing disinflation in used car and truck prices; these declined yet again even as auction price data from Manheim suggest a rise in auction prices in recent months.

This ongoing divergence poses the risk of a catch‑up increase in coming months, possibly worsening the inflation prints even as the upward impetus from energy fades. Alternatively, it could be that dealer margins in the used car market are being compressed as consumers become more price sensitive and unable to accept higher prices.

To be sure, real disposable income growth slowed quite dramatically to just 1.1% YoY in February. Aside from the big Covid‑related gyrations in 2022, this marked the slowest gain since 2014.

The implication is that pricing power must weaken in the context of weaker income growth. The inflation squeeze will hit real income further in March, although tax refunds will offer a cushion. This, in turn, suggests an eventual slowdown in real consumption.

Consumer sentiment is already taking a hit as a result of the energy price spike. The Michigan consumer sentiment index plunged another 5.7 points in March to a multi‑decade low while inflation expectations rose.

Short‑term (one‑year) inflation expectations rose one percentage point to an eight‑month high of 4.8% while long‑term inflation expectations ticked up two tenths to 3.4%.