A reminder and more data questions

We’ve spent much of the last couple of months highlighting the contradictory signals from different parts of the labor market, arguing that while the narrative of labor market stabilization is well supported, the narrative of a sustained reacceleration was not yet so.

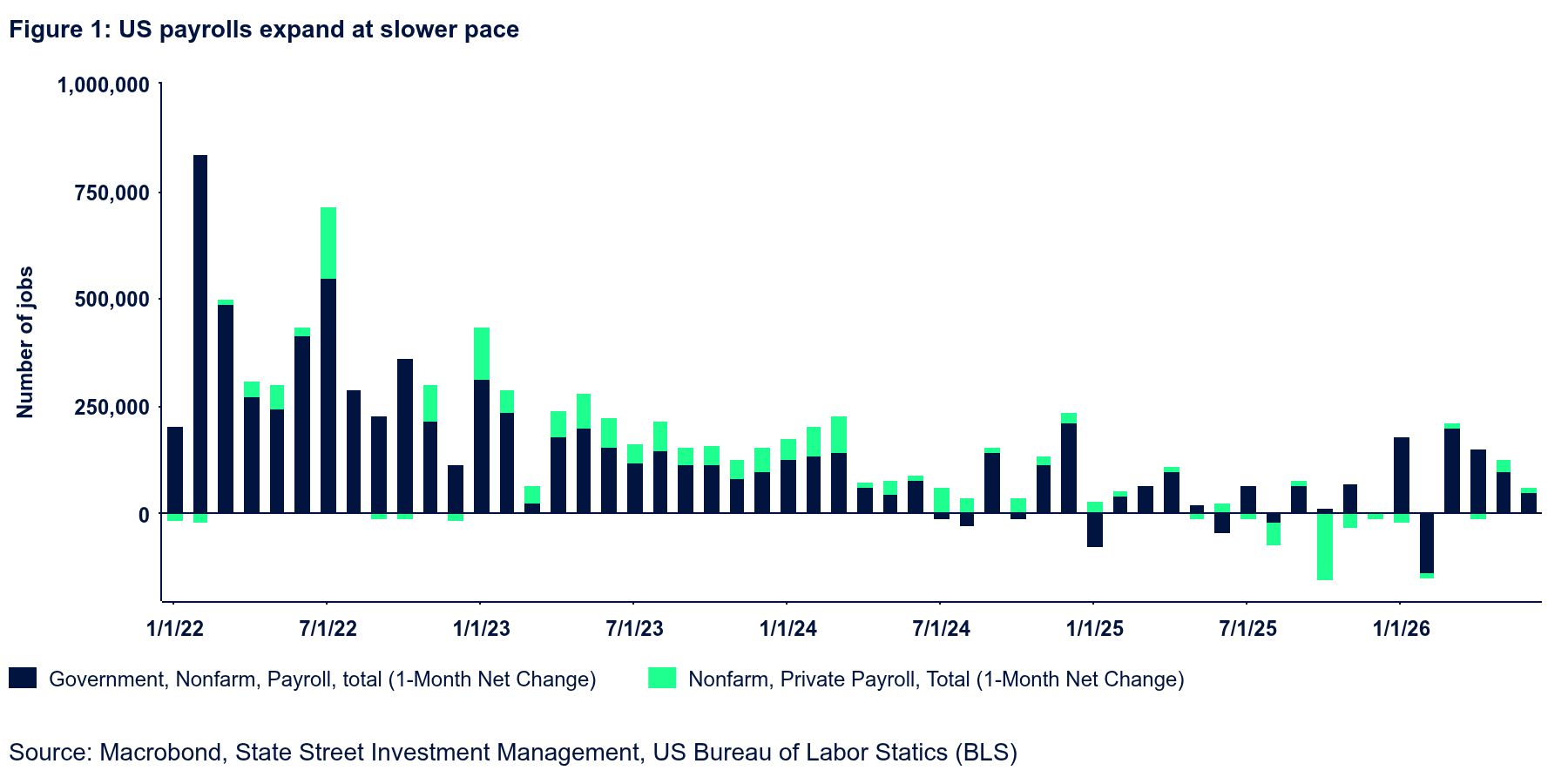

The June employment report demonstrated why. The economy added 57k in June, which was about half the expected number. The bigger caveat, however, was the 74k downward revision to the prior two months. In other words, the level of employment at the end of June was lower than we previously believed it to be at the end of May. Even so, the unemployment rate eased one tenth to 4.2%. This reflected an unusually sharp decline in the labor force participation rate, which retreated three tenths to 61.5%. The participation rate is down a full percentage point since September. The steep retreat in June reflected a 507k plunge in employment (as reported in the household survey) and a 213k plunge in unemployment, lowering the labor force by 720k. This is quite extraordinary and hard to explain. The prime age labor force participation rate plunged by 0.6 percentage points (ppt), the single largest monthly decline since January 1968 (outside of Covid). The suddenness and the magnitude of the move do not come across as credible, so, once again, we’ll need to await further details.

There were only two notable details in June’s sector distribution of job gains. Firstly, there was a 61k decline in leisure and hospitality employment, which makes sense given that surging travel costs likely hampered demand temporarily. It would not be surprising to see a rebound here in coming months. Secondly, the strength in state and local government employment that appeared so stark and so surprising last month has largely faded on account of big downward revisions and a soft print for June itself. This seems reasonable as well. Here, there is little reason to anticipate much of an improvement going forward.

Wage inflation remains contained, with total average hourly earnings inflation down a tenth to 3.4% YoY, the lowest since May 2021. This detail, in particular, should be reassuring to the FOMC. We maintain the recently revised call of a Fed on hold this year (previously we expected two cuts). Market expectations have turned a little less hawkish, but investors still price more than one full hike in 2026.