Hawkish jolt

The first FOMC meeting under Chair Warsh’s leadership marked a clear hawkish tilt in messaging, though perhaps not quite as hawkish as markets are pricing.

In line with our expectations, the Fed Funds rate was left unchanged at 3.50-3.75%, and the one rate cut previously embedded in the summary of economic projections was removed. The new “dot plot” was notably more hawkish, with 9 participants expecting at least one hike this year, while 9 others anticipated the policy rate to remain on hold or be lowered. The median dot implies one rate cut in 2027 and one more in 2028. Updated economic forecasts incorporated higher inflation, modestly lower growth, and incrementally lower unemployment rate in 2026.

Chair Warsh did not submit a dot. In the perfectly even distribution of the remaining ones, we can’t help but infer a bit of deference to the new chair as his dot—should he have chosen to offer it—would have tipped the scales in one direction or another. As things stand, we are left with anxious anticipation. There is no denying that the dot plot, the forecasts, the (drastically shortened) statement, and the press conference all were hawkish overall. But how hawkish? Hawkish enough to deliver a hike or two this year, as markets are currently anticipating? Maybe … maybe not.

While the focus of almost the entire press conference was on inflation, this should not be surprising. The mere speculation of a potentially compliant chair who would deliver rate cuts irrespective of economic conditions required Chair Warsh to take a stand to establish credibility. Secondly, recent data suggest there is not much reason to worry about the labor market. So, we focus and talk about the one area of concern, which is inflation.

Even so, the discussion about inflation was more nuanced in our view than what markets took it. While there was the clear promise that “the committee will deliver price stability”, Chair Warsh also talked about the need to understand what is driving inflation, and to make policy based on forward looking signals. He also noted that the “dots” can become obsolete very quickly at a time of rapid change, as is currently the case with the Iran conflict and oil prices.

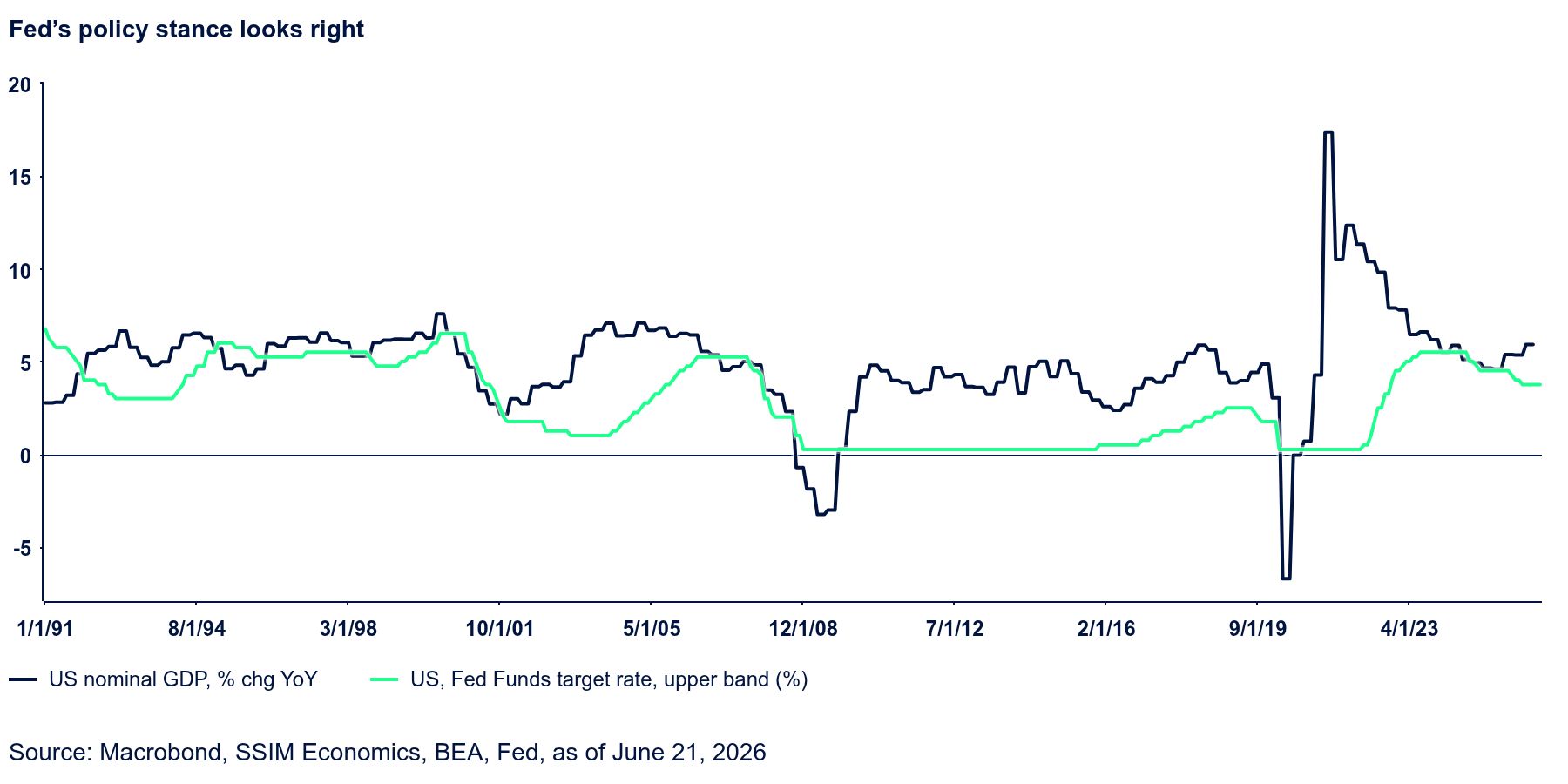

In our opinion, the Fed’s current policy stance is about right and could well end up being retained through year-end. The graph below shows that over the last two decades, nominal GDP growth typically exceeded the Fed Funds rate by a sizable margin. When it did not, recession followed. This was one key reason why last year, when that gap had disappeared, we argued in favor of multiple Fed rate cuts even in the face of tariffs. Those cuts have since re-established space. The point is not to rush and close it again…