K-shaped to the max!

The phenomenon of divergent performance across consumer segments (the so-called “K-shaped economy”) is intensifying.

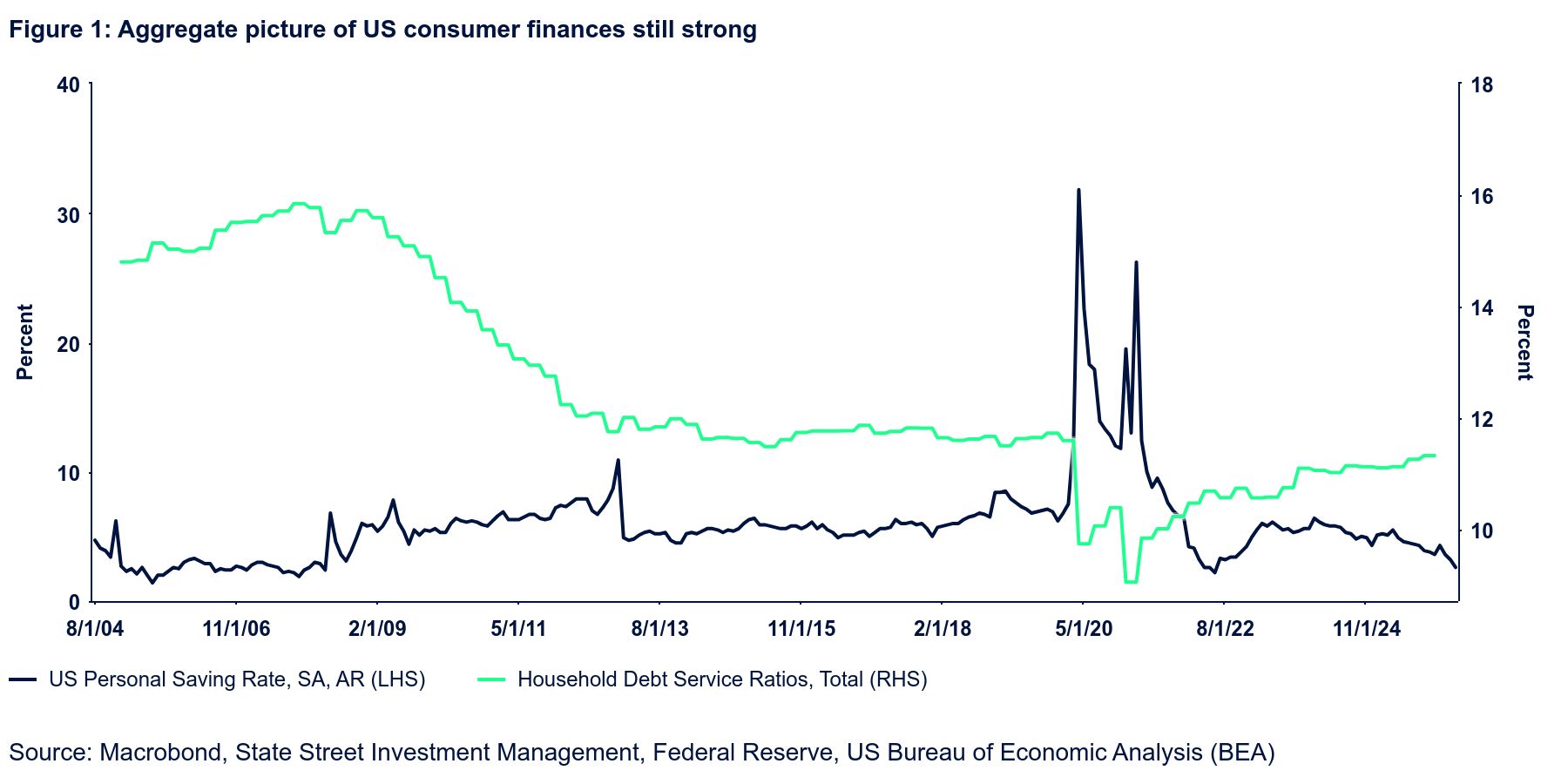

Aggregate data on consumer finances continue to show a robust picture. Debt service ratios have risen from pandemic “super lows”, but they have yet to fully return to the levels that prevailed in the late 2010s. Most importantly, they remain far below the pre-GFC peak (Figure 1, page 2). And although the personal savings rate fell to 2.6% in April (the lowest level since 2008 save for Covid!), the overall picture remains reassuring given record high household net worth.

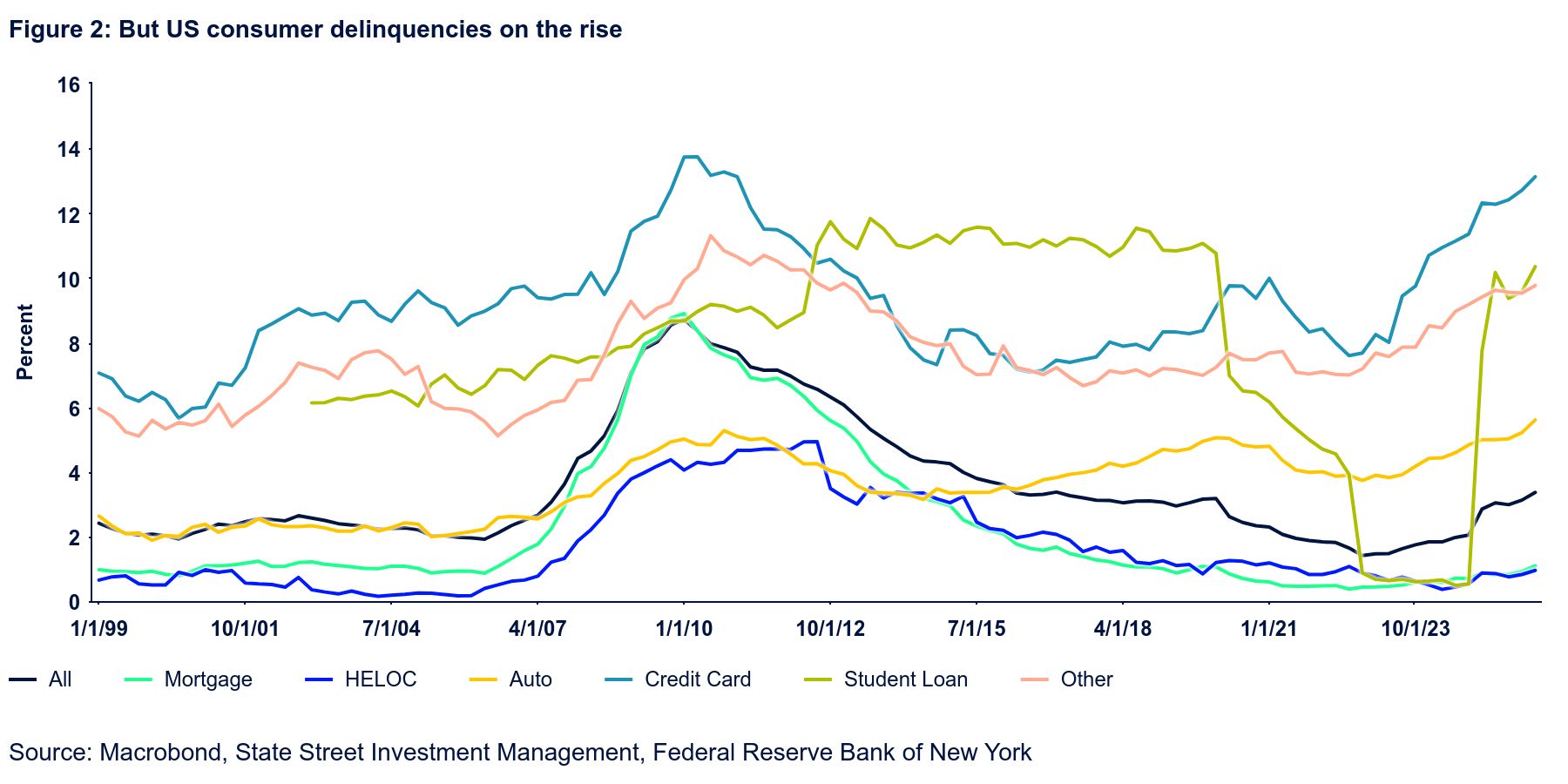

Troubling signs appear when looking below the surface. Despite a labor market near full employment, consumer delinquencies have been steadily rising for years (Figure 2). The delinquency rate on auto loans has hit a record high, credit card delinquencies are approaching the GFC highs, and even the long-dormant mortgage segment is now registering early signs of deterioration. Even in the context of a stable labor market, delinquencies may deteriorate further given tepid household income growth. Indeed, data released this week showed flat nomina income growth m/m and a 1.1% YoY decline in real personal disposable income.

Revised Q1 GDP data showed slightly weaker consumer spending growth during the quarter, which better fits the income growth trajectory. Real GDP grew 1.6% QoQ seasonally adjusted annualized in Q1, versus the 2.0% earlier estimate. We do expect overall consumer spending to slow to 2.0% this year, compared with 2.6% in 2025 and 2.9% in 2024. Any deterioration in the employment picture would represent material downside risks to this forecast.

The weak income growth and rising delinquencies combo also implies a much more constrained pricing power environment than in 2022 during the height of the supply chain-related inflation surge. We see limited second-round effects from the energy price shock.