Hotter inflation prints reignite rate hike debate

There is no denying that the April inflation data came in pretty hot. Consumer price inflation accelerated another half a percentage point to 3.8% YoY, the highest read since May 2023. Much of this reflected ongoing increases in energy prices, with energy commodities now up 29.2% YoY. For comparison, the same category printed -5.2% YoY as recently as February!

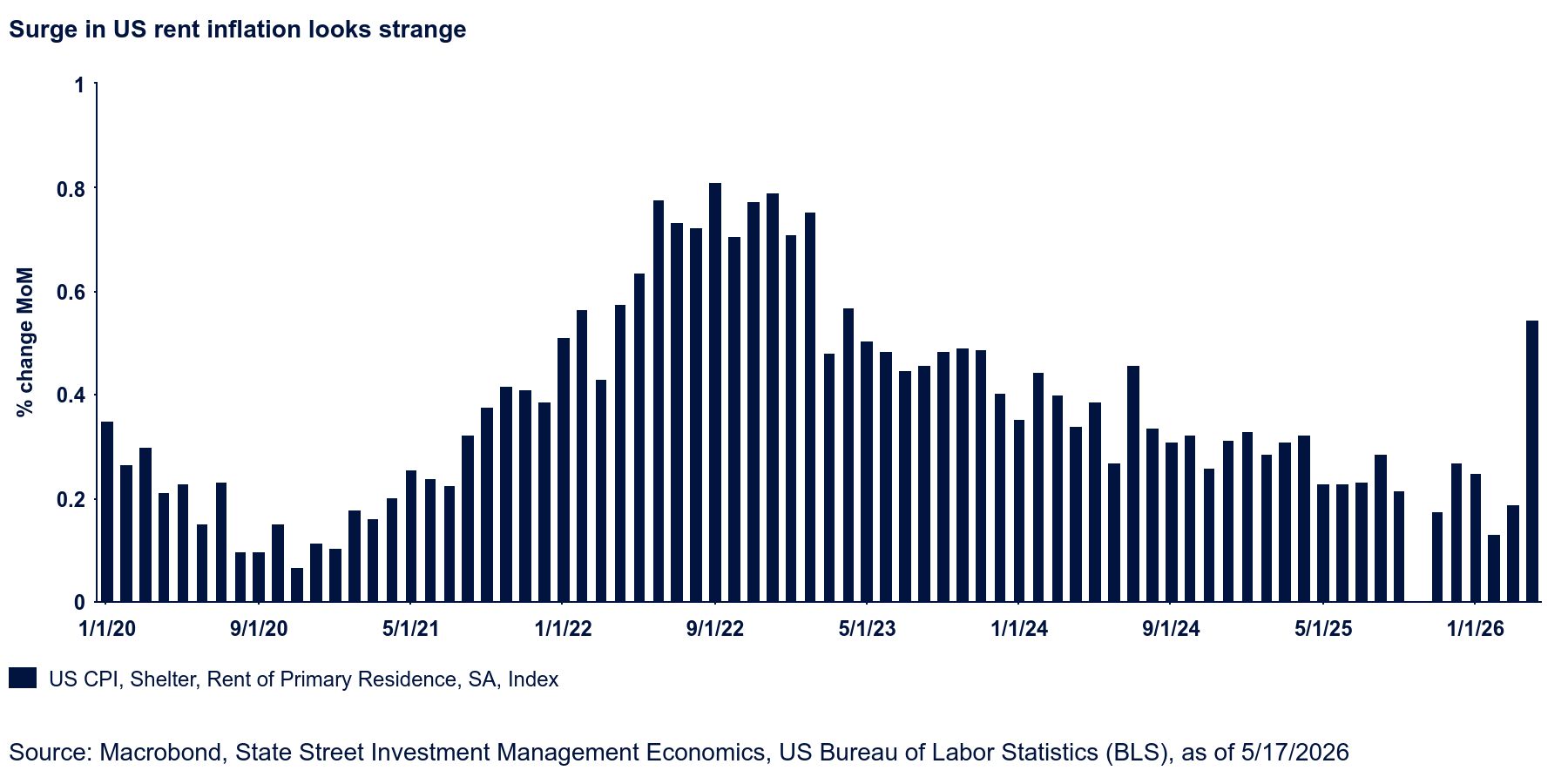

However, the real surprise was the 0.6% MoM increase in services, in turn driven by an outsized 0.6% MoM surge in shelter. This lifted core price 0.4% MoM and lifted core inflation by two tenths to a six-month high of 2.8% YoY. By contrast, the other service categories (even transportation) were well-behaved.

Our more constructive view on inflation incorporates expectations of ongoing shelter disinflation, so the April update was indeed a challenge to that assessment. Nevertheless, we find the data unconvincing because it lacks corroboration in other indicators. As such, we see the hot April print more like an outlier than the start of a new trend. Why do we say this? Firstly, the magnitude of the increase is just so completely out of the recent context; even when taking into account some possible sample-related issues, the gain just seems exceedingly large.

Meanwhile, market data for rents from sources such as Zillow or Apartment List do not indicate any inflection higher in rents so far. Additionally, the rental vacancy rate continues to climb higher, and this is generally a very good leading indicator of future rent inflation. For instance, the national rental vacancy rate hit 7.3% in the first quarter, the highest since Q3 2017. Given real personal disposable income is barely rising, it seems unlikely that landlords would be able to push through significant rent increases. There is not much to do but wait for more data to gain clarity. Until then, we are tempted to dismiss this as more noise than signal.

That being said, both producer prices and import price data came in hotter than expected, largely (but not entirely) driven by energy prices. In terms of import prices, we are struck by the two large consecutive monthly increases in import prices from China, which stand in stark contrast to the behavior seen a year ago around tariff liberation day. We question how much more upside is here.

The hot inflation wave has once again pushed market expectations in a hawkish direction, with odds of a Fed hike this year now above 50%. We are not surprised to see that happen, but we believe the threshold for a hike is extremely high. There were so many apparent anomalies in this batch of inflation data that we could easily see some reversals soon, in which case market expectations could shift once again. Our confidence in our call for two rate cuts late this year has certainly diminished, but we are holding on to that call until at least the next batch of inflation updates. If the upward momentum persists, a reassessment will be in order.