Better labor market news

We can easily outline two very different narratives around the US labor market, but it is fair to say that last week’s data flow was more supportive of the constructive view. Payrolls rose by a much better than expected 115k in April, and the prior two months’ downward revision was minimal. The average workweek lengthened by six minutes and aggregate hours worked (a measure of aggregate labor effort in the economy) increased a decent 0.3%. Wages were in the goldilocks zone: not cool, but not too hot. The unemployment rate was steady at 4.2%. What’s not to like?

Well, we did like the report, and what we liked even better is that it appears to be corroborated by modest improvements elsewhere, such as unemployment claims, the JOLTS report, where the hiring rate rebounded sharply. Stabilizing labor market conditions are also mirrored in the Conference Board labor differential (which measures the difference between consumers who feel jobs are “plentiful” and those who feel jobs are “hard to get”). That number bottomed out at 5.7 in February and has since improved to 7.5; this is still a rather abysmal level historically speaking, but there is at least a sense that things are not getting worse. And that’s worth something.

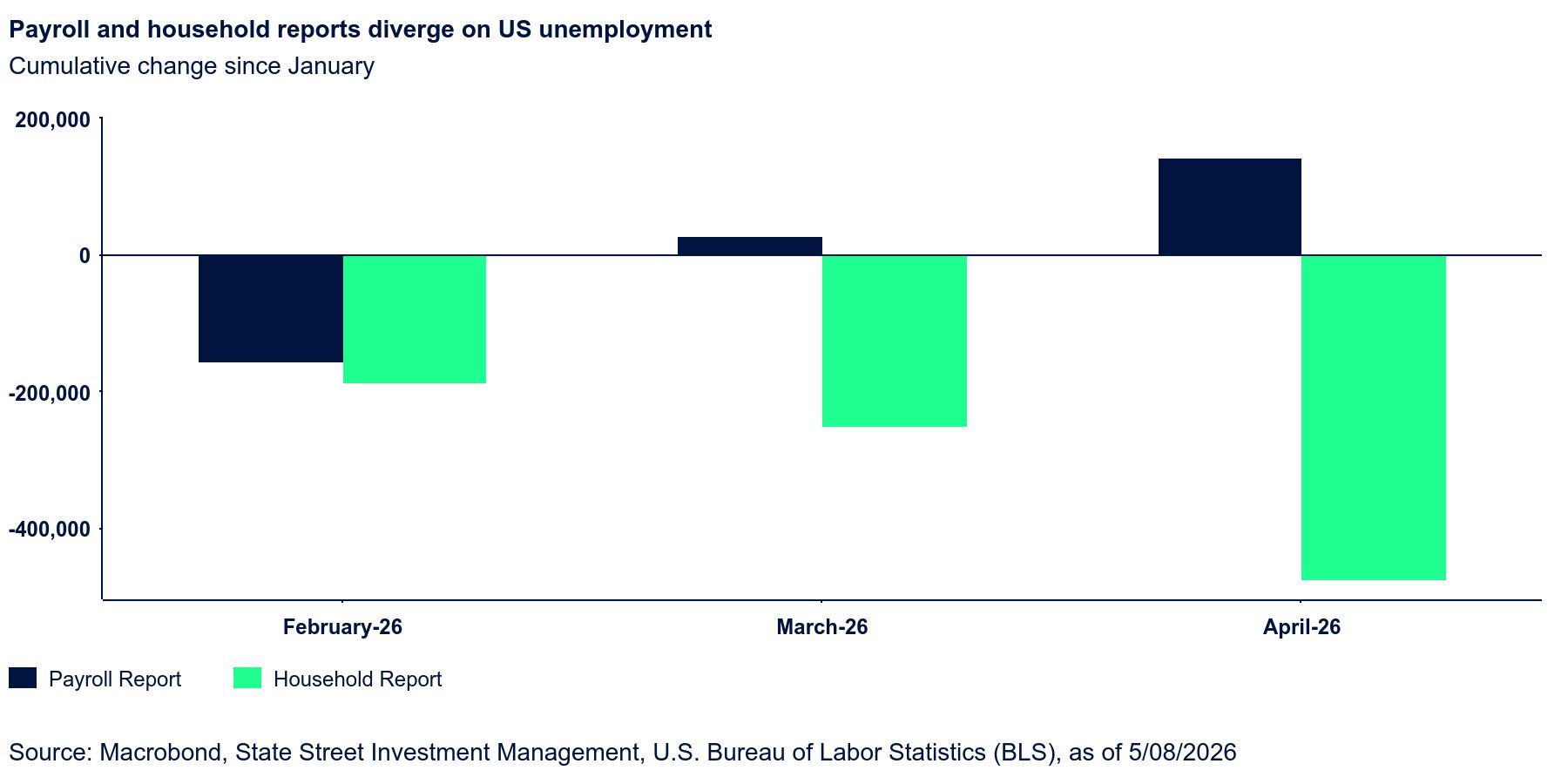

Yet it is definitely not worth betting the house just yet on a labor market revival narrative. It is far too soon for that. The truth is, the totality of the data still sends mixed signals. Take, for example, the growing divergence between the payrolls and household reports. Compared with the January levels, the payrolls report shows a cumulative employment gain of 144k, whereas the household report shows a cumulative loss of 475k, a sizable discrepancy that widened especially in March and April. While it is not unusual for these two measures of employment to differ, the divergence at the very least cautions us to take the payroll gains with a grain of salt, at least for the time being.

We also struggle to tie the dramatic reduction in the labor force participation rate over the last six months to any specific development. Since the recent peak in September 2025, the labor force participation rate has dropped 0.7 percentage point; a decline of such magnitude over such a short timeframe was only previously experienced during Covid, in 2009, and very briefly, in 2001. The drop in participation is what has helped cap the unemployment rate so far, but should that pick up without a commensurate increase in hiring, we could still see the unemployment rate rise in coming months. We continue to watch this space.

What does this mean for our Fed call of two cuts in September and December? The apparent labor market resilience undermines somewhat a core argument in favor of hikes, but given the timing, we do not yet feel compelled to adjust the call.