Fed on hold as outlook turns more binary

The April Fed meeting was not about doing but about signaling. The decision on rates was always a given: don’t do anything while you await clarity on what you might have to do down the line. So, the Fed Funds rate stays at 3.5–3.75%. There was one dissent (Miran) in favor of a 25 bp cut and three dissents (Hammack, Kashkari, Logan) against statement language implying an easing bias. In other words, while Chair Powell left the door open for future cuts, other committee members are drawing the battle lines around the future debate on rates. The outlook is indeed becoming more binary given Iran-related inflation risks.

The most important reminder from the press conference was that monetary policy is made through the “collective judgment of the committee.” The Chair has only one vote, even if one carrying more weight than the others. The nature of the current economic moment essentially guarantees that the policy debate will intensify (publicly) in coming months. Presumed future Chair Warsh’s first order of business will be to find the middle ground within the FOMC, and that means holding rates steady for a while.

That being said, we still hold to our call for two cuts this year, in September and December. But it all depends on whether our core assumptions of a material de-escalation in hostilities by the latter part of May, the resumption of oil traffic, and subsequent pullback in energy prices are validated by future events.

Meanwhile, incoming data highlight an economy that is quite resilient, even if not firing on all cylinders. Advance estimates (which are prone to material revisions) show real GDP grew at a 2.0% seasonally adjusted annualized rate (SAAR) in the first quarter, exactly in line with the 2025 average. There was some bounceback in government consumption following the shutdown, a very slight slowdown in consumer spending, a jump in private fixed investment, and a widening of the real trade deficit as imports surged a lot more than exports.

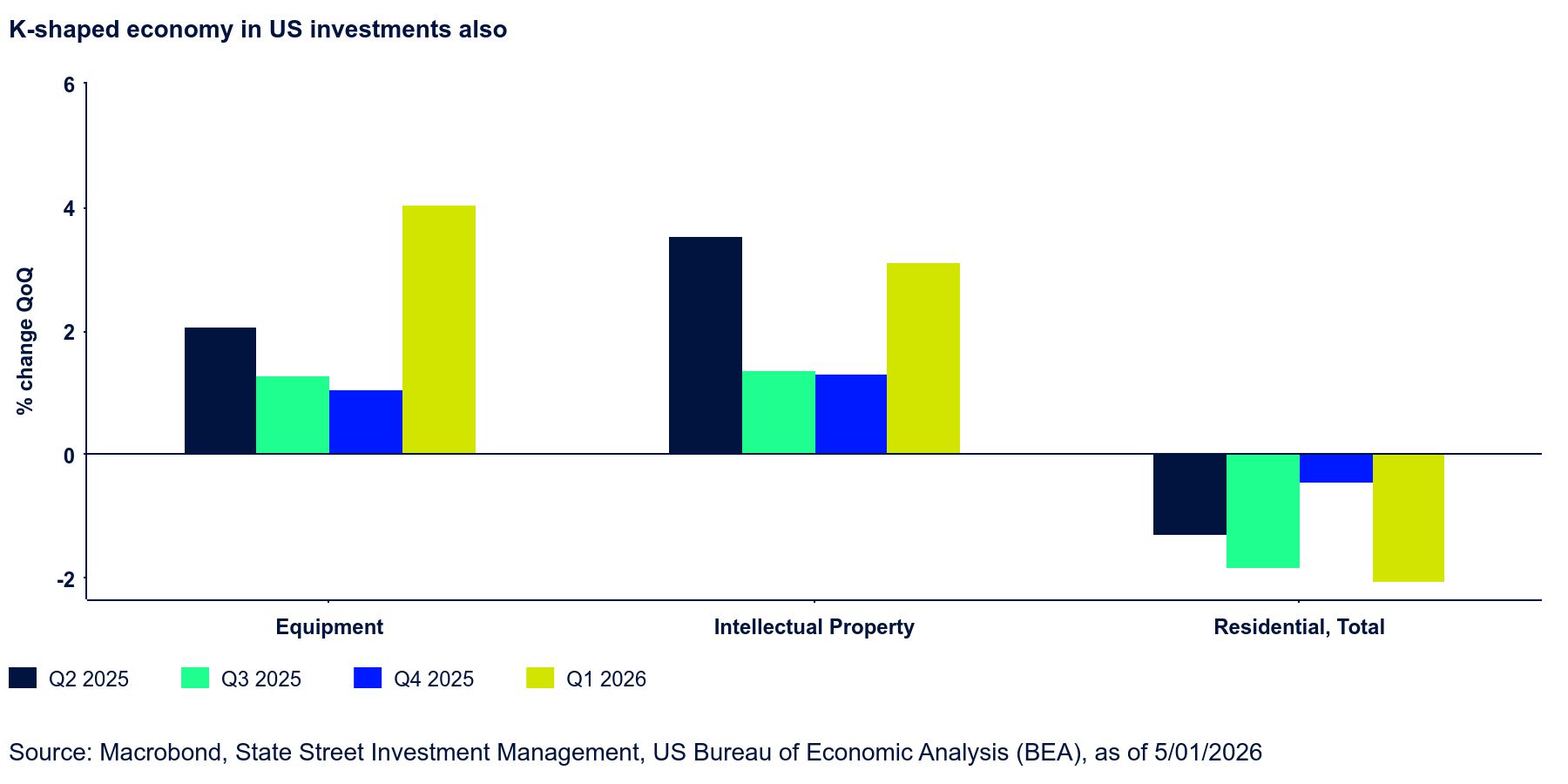

There is tremendous divergence within the broad categories, however. Within consumption, real goods consumption was flat, so all the spending growth is happening on the services side. In private fixed investment, the residential segment shrank sharply—in fact, at the fastest rate since end‑2022.

Nonresidential structures also contracted, but equipment and IP investment soared and are up 8.7% and 9.7% YoY, respectively. There is little evidence from company earnings that activity is pulling back here, but it would be surprising to see a repeat of this performance given the larger comparison base.

On that point, data on construction spending (value put in place) show data center construction overtaking overall office construction for the first time in November 2025 and continuing to do so through January.