Softer growth, hotter inflation signals

Revisions to Q4 GDP delivered a softer read on consumer spending. This was not particularly surprising; in fact, it had been the previously reported resilience in services spending that seemed odd to us given tepid labor market conditions and modest income growth. Thus, the new update simply puts spending on a path more consistent with income growth. It is not yet fully consistent, given that real spending growth continues to outpace real income growth, but the divergence has narrowed.

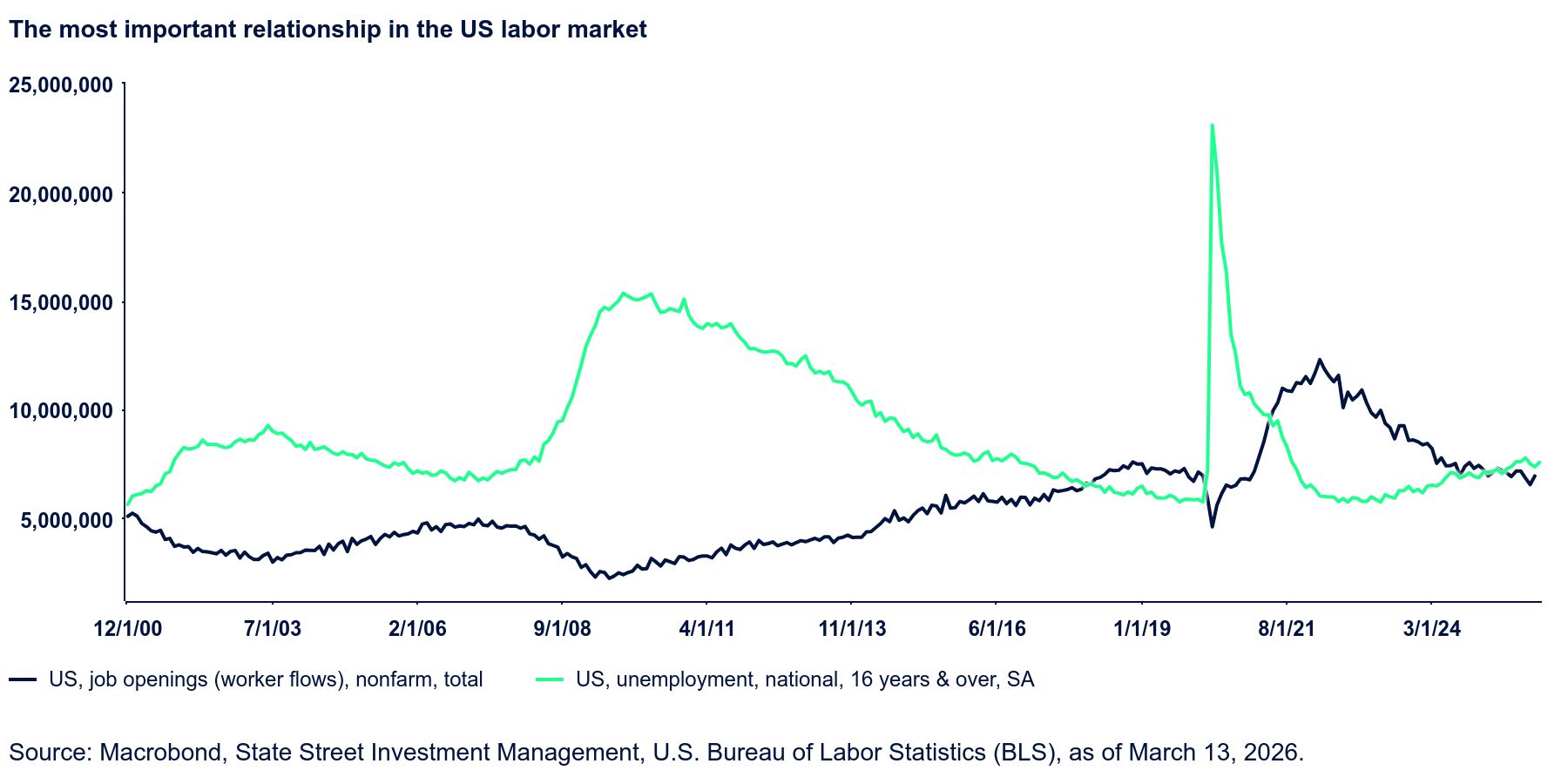

This is a reminder that the health of the labor market remains the critical lynchpin to the household balance sheet health, consumer spending sustainability, and overall growth. Despite an upside surprise in job openings in January, the overall trend in the labor market is towards softening. Moreover, the January job opening update, showing an almost 400k jump in openings, seems a little odd given it was so heavily driven by very large firms, which one would presume might be at the forefront of labor-saving AI deployment. Other forward looking signals of labor demand were softer: for instance, the “hiring plans” component of the NFIB small business survey slid four points to 12 in February, its lowest level since May.

For the time being, all eyes are on the Iran conflict and the dominant angst in the marketplace is that this is an inflationary shock that may prevent further Fed easing this year. Indeed, having priced about 2.6 rate cuts from the Fed just a few short weeks ago, the latest market pricing is for barely one cut. This seems reasonable for now given the genuine risks of extended conflict and lasting damage to oil infrastructure and supplies. However, it is not the only scenario, nor the only concern; labor market weakness could—and likely will—gain prominence again in coming months. For now, there is no compelling reason for the FOMC to change the core signal from the December dot plot that indicated one rate cut in 2026. While individual dots may change, we expect the median dot to continue to signal the same. For our part, despite uncertainties around the Middle East conflict, we see room for more easing in the latter part of the year. Our call for three Fed rate cuts is under threat but has not been irreversibly damaged just yet.