Slowdown into year-end

Following torrid growth in the second and third quarters, real GDP growth slowed markedly in the fourth under the combined influence of the government shutdown and a greatly diminished contribution from trade.

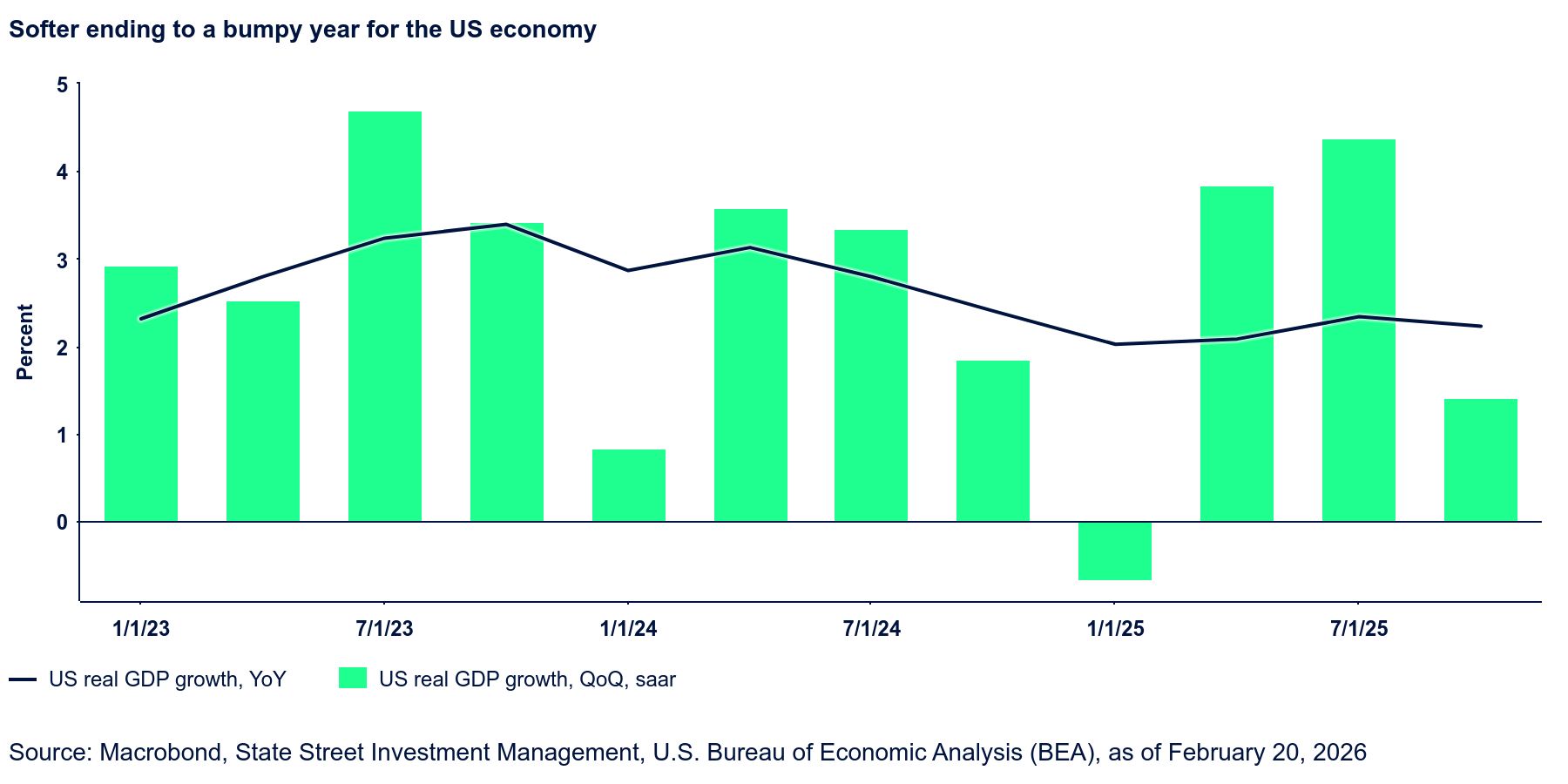

Real GDP grew at a seasonally adjusted, annualized rate of 1.4% in the fourth quarter, down from 4.4% in the third. On the positive side of the ledger, personal consumption contributed about 1.6 percentage points (ppts), fixed investment contributed 0.45 ppts, and inventories added 0.21 ppts. Net exports were almost neutral, having boosted Q3 growth by 1.6 ppts. Government spending detracted 0.9 ppts, having added almost 0.4 in the third quarter. Evidently, with the extensive government shutdown over, there will be some bounce-back here in Q1.

Real GDP grew 2.2% in 2025, moderating from 2.8% in 2024 and 2.9% in 2023. We look for growth of around 2.5% this year. Performance is likely to remain bumpy throughout the year as base effects and policy changes will impact firm behavior.

A case in point is the Supreme Court decision that rendered the IEEPA tariffs imposed on April 2 unconstitutional. We anticipate that the administration will move swiftly to deploy tariffs utilizing alternative avenues—albeit at a lower weighted rate—such that the impact on economic activity and inflation over the course of the year would be somewhat muted. Nevertheless, as policy parameters shift, we are likely to see firms actively managing import flow in a way that could lead to considerable skews in performance from quarter to quarter.