The long wait for the resumption of Fed rate cuts may be soon over. Almost irrespective of the next payrolls report, there is enough softness in broader labor market data to warrant a modest reduction in the Fed Funds rate.

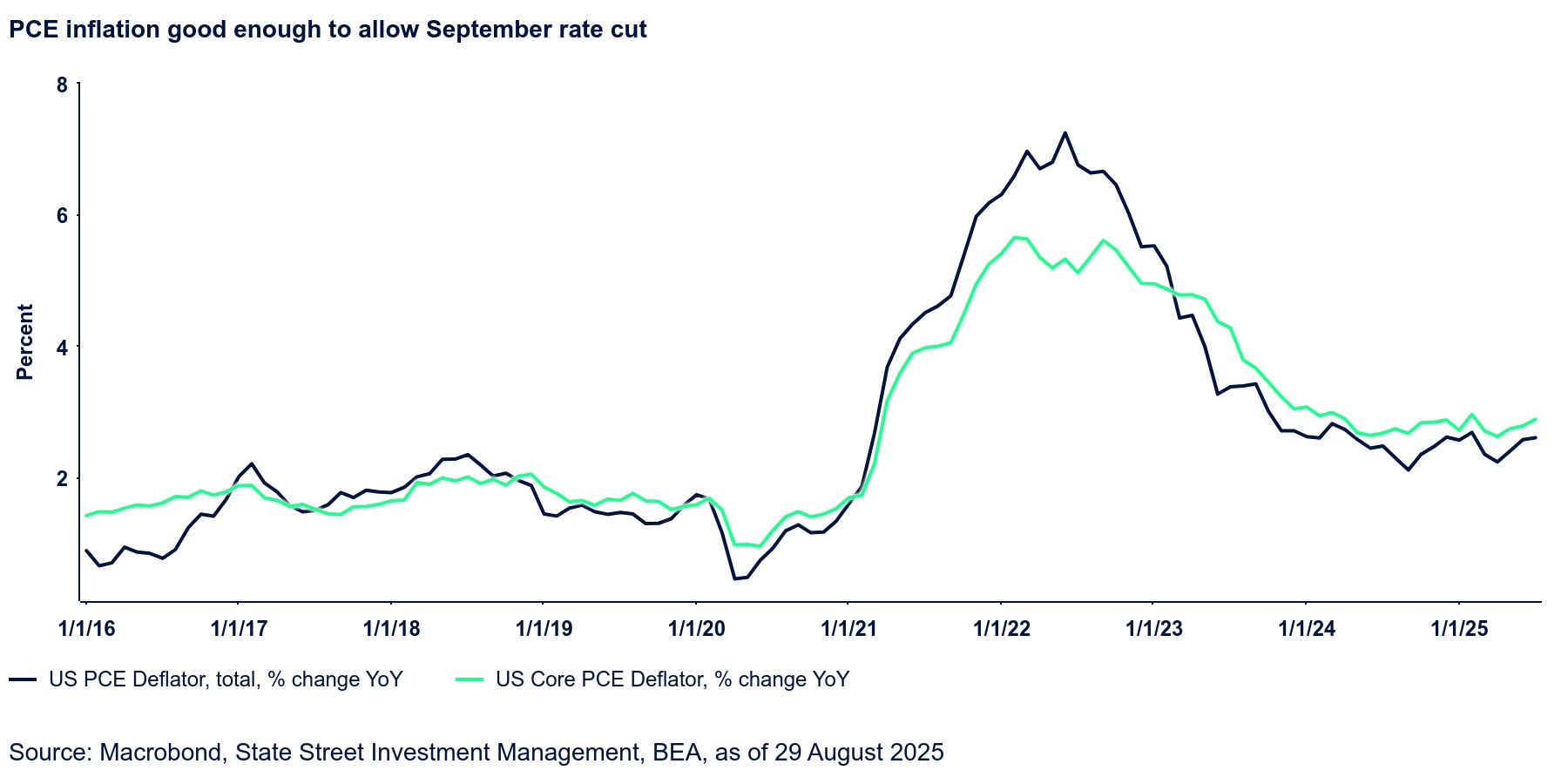

Whatever objections there are to such a move center on the reality that inflation is not yet at target, nor is it likely to get there very soon. That is undeniable, as Figure 1 below illustrates. The latest PCE (personal consumption expenditure) inflation data were, at the margin, more constructive than we anticipated, but with headline at 2.6% and core at 2.9%, we are a way away from the ideal end point. We will probably get even further away from it before the year is over.

Why, then, do we support a rate cut in September (we’ve argued in favor of a July cut as well) and a total of three in 2025?

In short, because at the September meeting, the Fed is truly making policy for the middle of 2026, and we put more weight on growing labor market vulnerability. On one hand, it is impressive how well the economy has performed despite the many policy shocks of the last few months. But it is also clear that consumer spending is slowing. It grew 0.3% QoQ on average during the first half of 2025, half the pace of a year earlier.

Keeping it growing rests on ensuring that the labor market does not transition from the current phase of slow hiring to outright firing. And we believe that calibrating interest rates lower is critical to prevent that shift from happening and/or taking hold.